Delivering the AUKUS Advanced Capabilities Industry Forum (ACIF) during Farnborough Airshow

Delivering the AUKUS Advanced Capabilities Industry Forum (ACIF) during Farnborough Airshow

Last week, the UK was proud to host the first in-person AUKUS Advanced Capabilities Industry Forum (ACIF) for 2026 on the margins […]

Read more

ADS South West Making a Difference Awards 2026 – Nominate Today

ADS South West Making a Difference Awards 2026 – Nominate Today

Applications are now open for the ADS South West Annual Making a Difference Awards 2026, and we invite you to showcase your […]

Read more

ADS Charity Cycle: A conversation with Combat Stress

ADS Charity Cycle: A conversation with Combat Stress

This summer, we’re trading desks for pedals as we take on an epic 350-mile cycle challenge from Belfast to Bristol, passing through […]

Read more

Wiltshire schoolchildren take on USA, Japan, Ukraine and France in international rocketry final

Wiltshire schoolchildren take on USA, Japan, Ukraine and France in international rocketry final

Farnborough (24 July 2026) – A team of students from Abbeyfield School in Chippenham has been crowned the winners of this year’s […]

Read more

£62.9 billion in aircraft deals done at Farnborough International Airshow 2026, according to ADS Group

£62.9 billion in aircraft deals done at Farnborough International Airshow 2026, according to ADS Group

£62.9 billion ($84.7 billion) of deals have been made on during the first four days of Farnborough International Airshow 353 firm […]

Read more

Trade association ADS signs Cooperation Agreement to strengthen aerospace engineering standards

Trade association ADS signs Cooperation Agreement to strengthen aerospace engineering standards

ADS and SAE International sign Cooperation Agreement to strengthen UK aerospace industry engagement in global standards development The agreement will give […]

Read more

First-ever UK-Taiwan drone industry collaboration established at Farnborough Airshow

First-ever UK-Taiwan drone industry collaboration established at Farnborough Airshow

Farnborough (23 July 2026) – ADS, the trade association representing the UK’s aerospace, defence, security and space sectors, and the Taiwan Excellence […]

Read more

Hyde achieves two gold aerospace supply chain awards at Farnborough International Airshow

Hyde achieves two gold aerospace supply chain awards at Farnborough International Airshow

Hyde Details and Hollygate Aircraft Components have both received their first Gold Supply Chains for the 21st Century (SC21) awards The award […]

Read more

ADS and UK-India Business Council sign collaboration agreement at Farnborough Airshow

ADS and UK-India Business Council sign collaboration agreement at Farnborough Airshow

ADS and the UK-India Business Council (UKIBC) have signed a Strategic Collaboration Agreement to strengthen UK–India defence and aerospace industrial partnerships The […]

Read more

82 firm aircraft orders made on Day Two of Farnborough International Airshow, ADS finds

82 firm aircraft orders made on Day Two of Farnborough International Airshow, ADS finds

Farnborough (21 July 2026) – The second day of Farnborough International Airshow has generated £16.4 billion ($22.1 billion) of aircraft deals, […]

Read more

UK and Japanese trade associations sign collaboration agreement in defence

UK and Japanese trade associations sign collaboration agreement in defence

Trade associations ADS (UK) and SJAC (Japan) sign MoU to strengthen UK-Japan defence industrial collaboration The signing took place during the […]

Read more

ADS welcomes Prime Minister Rt Hon Andy Burnham

ADS welcomes Prime Minister Rt Hon Andy Burnham

Kevin Craven, CEO of ADS Group, welcomes the new Government: The first day in a new job is a perfect time […]

Read more

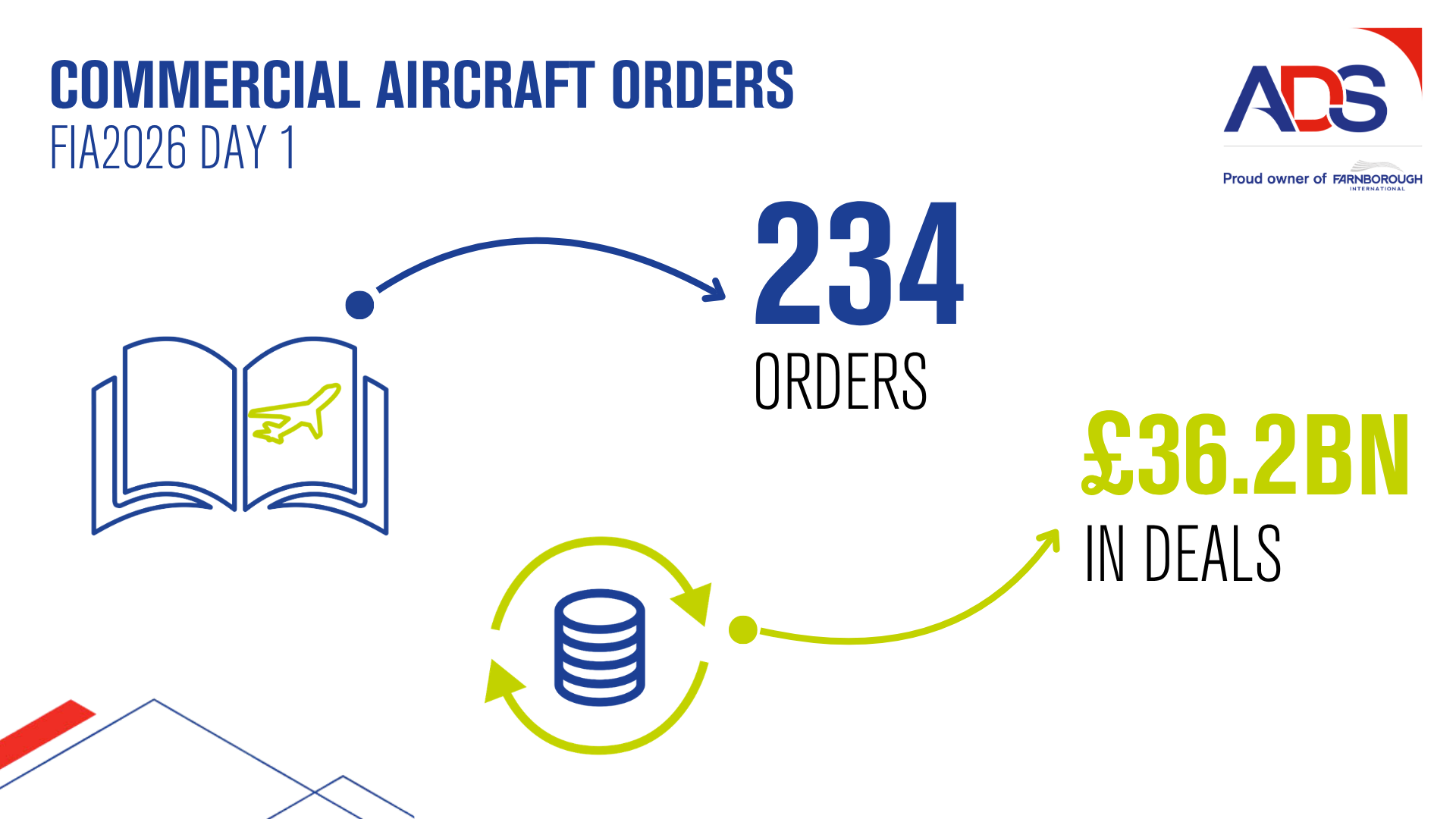

£36.2 billion in deals done on Day One of Farnborough Airshow, according to ADS Group

£36.2 billion in deals done on Day One of Farnborough Airshow, according to ADS Group

£36.2 billion ($48.8 billion) of aircraft deals have been made on day one of Farnborough International Airshow 234 firm aircraft orders […]

Read more

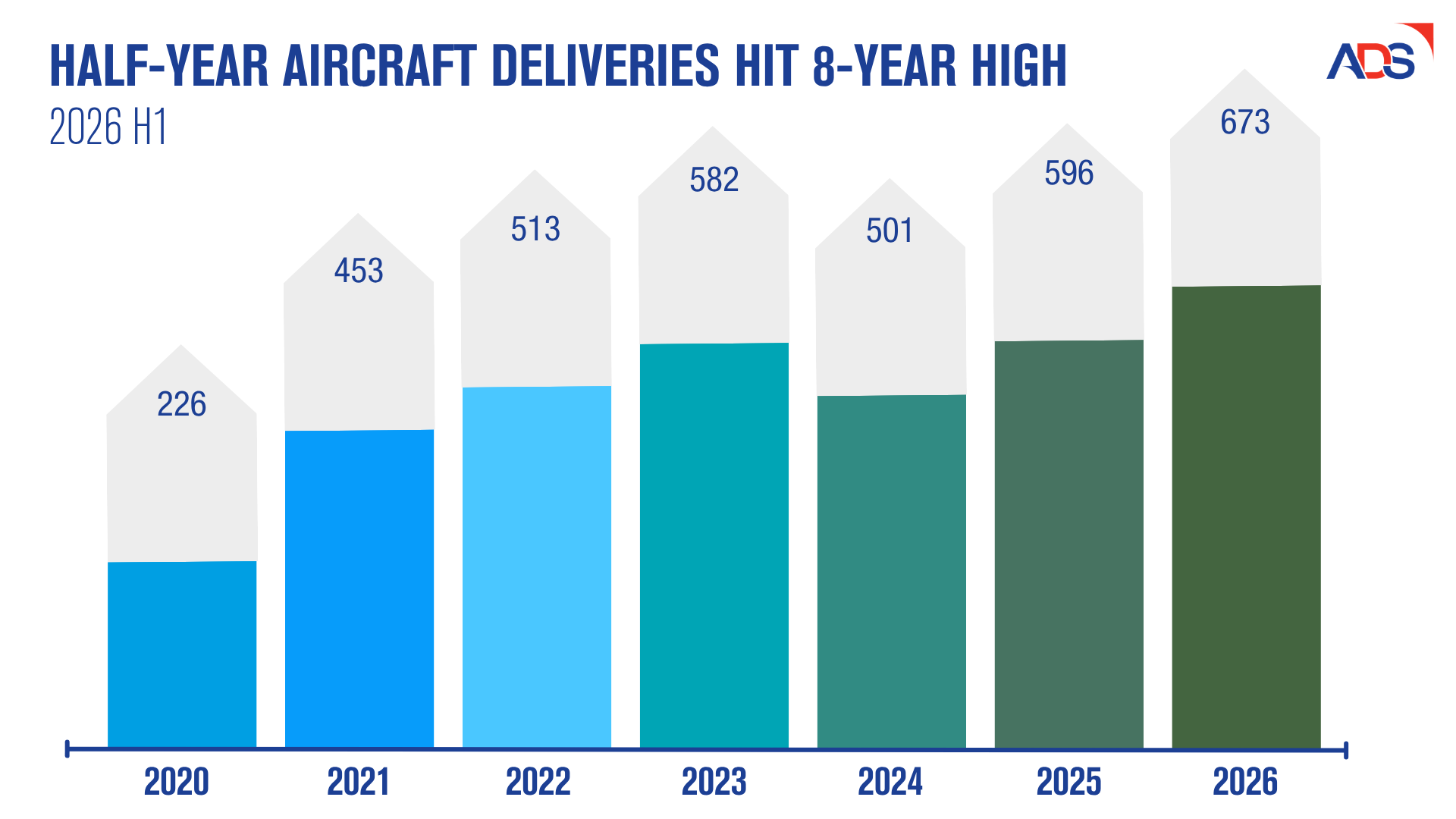

Half-year aircraft deliveries hit 8-year high, ADS finds

Half-year aircraft deliveries hit 8-year high, ADS finds

673 aircraft were delivered in the first six months of 2026, representing the highest half-year delivery total since 2018 Over the first […]

Read more

Trade association ADS surpasses 2,000 member organisations

Trade association ADS surpasses 2,000 member organisations

The trade association representing the UK’s aerospace, defence, security and space industries has reached 2,000 members More than 400 organisations joined […]

Read more