This morning the media were hailing ‘more good news’ as the UK is officially out of recession having achieved 15.5 per cent growth in Q3 compared to Q2. This is impressive growth figure, in fact the highest on record, but for those of you thinking ‘that recession didn’t last long’ don’t be sure that growth rates like this will last either.

The Q3 whole economy growth comes from a lower base in Q2 and includes the months July, August and September where the economy was reopening, we were eating out to help out and heading to the shops after months of sitting on the sofa, things were starting to feel a little like normal.

The growth rates were somewhat expected following a record decline in the UK economy in April. However, regional and local restrictions have in place from the end of September onwards and in England we now have a National lockdown as I write this in November, which will interrupt further growth. We can’t expect Q4 to reach these levels of growth even with Christmas coming up, expenditure remains way below 2019 levels with Q3 2020 9.6 per cent below Q3 2019.

Where is the growth?

As always, our interest and the interest of our membership lies in understanding where growth is coming from in the UK economy, and if our sectors are a part of it.

The good news is that services, production and construction output in Q3 2020 all saw record growth, again reflecting a reopening of the economy and ease of Q2 restrictions. The relaxing of the lockdown rules in Q3 unleashed some pent-up consumer demand but across the board activity and output remains below pre-pandemic levels. Public admin and defence output remains fairly constant throughout this.

Production in Q3

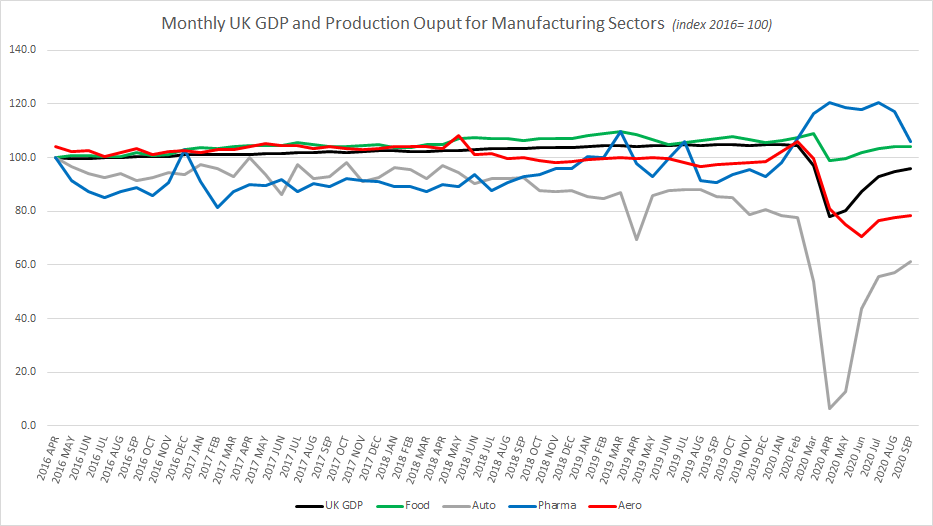

Production output in Q3 2020 grew by 14.3 per cent, not quite making up for the 16.3per cent decline in Q2 2020. This is a running theme through the data, significant growth but not enough to level out following record declines in Q2 2020. So broadly, the majority of sectors still have smaller output levels than they did In February 2020.

12 out of 13 manufacturing subsectors saw growth in Q3, and overall manufacturing output grew by 18.7 per cent. However, this remains less than the 21.1 per cent decline suffered in Q2 2020. The only area of manufacturing not to grow this quarter was pharmaceuticals which has seen significant growth rates in previous months due to increased demand that has now calmed slightly.

The quarterly breakdown for various areas of manufacturing saw a 3.8 per cent decline in pharmaceuticals index of production, a 175.5 per cent increase in Q3 2020 for automotive following plant shutdowns in Q2 creating a low base, food manufacturing saw a 3.7 per cent increase in output and with the slowest growth, Aerospace experienced just 2.7 per cent Q3 2020 growth on Q2 2020.

Aerospace slow recovery with no support in sight

The minimal growth of 2.7 per cent in Q3 2020 for aerospace manufacturing does not come anywhere close to a recovery from the -26 per cent decline seen in Q2 2020. The sector, including repair and maintenance services, is 29 per cent below February 2020 output levels.

Aerospace is without a doubt a sector that has been hardest hit by the pandemic, current border closures, quarantine periods and a lack of testing at airports are compounding the slow recovery of the sector compared to other areas of the economy.