The latest UK economic data is in, and there’s cause for cautious optimism beneath the headlines. UK GDP rose by +0.4% in the month of June, securing Q2 growth at +0.3% compared with Q1. While this is slower than Q1’s +0.7%, it’s still a better performance than earlier, gloomier predictions.

Looking at the first half of 2025, the UK economy has shown resilience in the face of ongoing uncertainties. Growth for the first six months of the year was +1% with strong contributions from services, +0.4%, and construction, +1.2%, while production experienced a rollercoaster ride. Geopolitical events and behaviours impacting in the UK resulted in a weak April and May for products that rebounded sharply in June to +0.7% growth. This uneven pattern highlights both the challenges and adaptability of UK industry with manufacturing driving the production rebound as it grew +0.5%, with 8 of 13 subsectors posting gains.

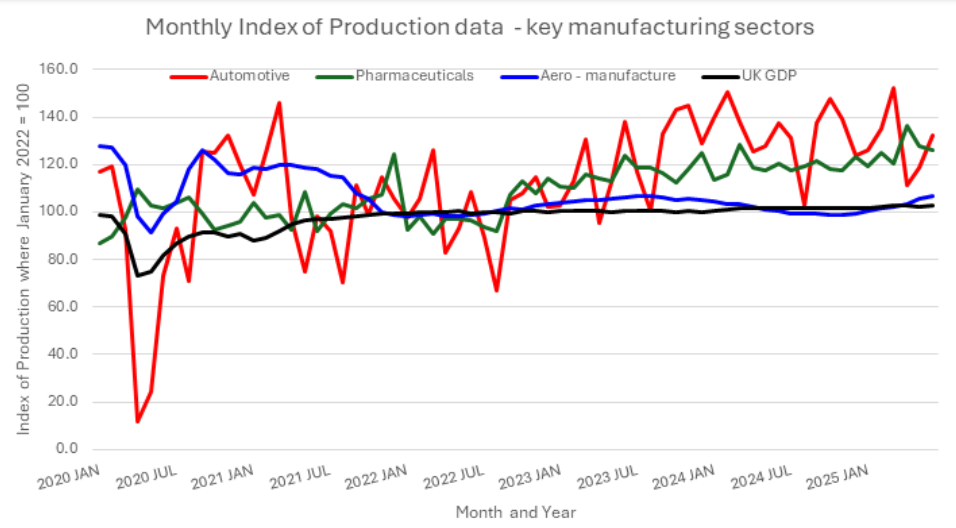

Aerospace Industry Pulling Its Weight

Within manufacturing, aerospace is a key contributor to the upward momentum with year-on-year growth of +3.9%, and consistent monthly gains since December 2024. Meanwhile, aerospace maintenance, repair and overhaul (MRO) rebounded +12.6% year-on-year, in June 2025, bouncing back from April’s dip.

In June 2025, almost every subsector made a noticeable contribution—positive or negative—to monthly production, except for computer, electronic, and optical products, which saw a whopping +8.8pp boost. Aerospace production index is performing closely in line with UK GDP, and monthly figures are far less volatile than other similar advanced manufacturing sectors.

What’s Driving the Trend?

ONS data points to defence-related demand as a key factor. Aircraft, weapons, ammunition. This helps to explain the contribution from electronics, which underpin cutting-edge systems in these industries.

For aerospace, the story is equally encouraging. Manufacturing growth aligns with steady global aircraft deliveries despite geopolitical headwinds, while the global order backlog topped 16,000 aircraft at the mid-year point of the year.

Looking Ahead

The outlook for Q3 is positive. Aircraft manufacturing is set to keep climbing, driven by a strong backlog, and MRO activity looks set to remain robust.

However, risks remain, with enhanced cost pressures, and the rollout of the UK-US trade deal (including aerospace parts exemptions) which could shake things up, but the outlook and the trajectory is upward.

The first half of 2025 paints a picture of a UK economy that is steady but not spectacular, with aerospace and defence sectors providing a crucial lift. As we move into the second had of the year, our industries will remain key to keeping growth on track despite broader economic vulnerabilities.